What is the Difference Between a Holding Company and an Operating Company?

When it comes to structuring businesses, the difference between holding companies and operating companies is a bit like the difference between a landlord and a tenant. One collects rent in their robe, the other unclogs the toilet at 3 a.m. The lines between them blur for the uninitiated, but here at hold.co, we know you’re not here for beginner tips—you’re here to dissect these entities with surgical precision (while enjoying the occasional sarcastic jab). So, let’s dive in.

The 30,000-Foot View (For Those Who Claim They Already Know)

What Is a Holding Company?

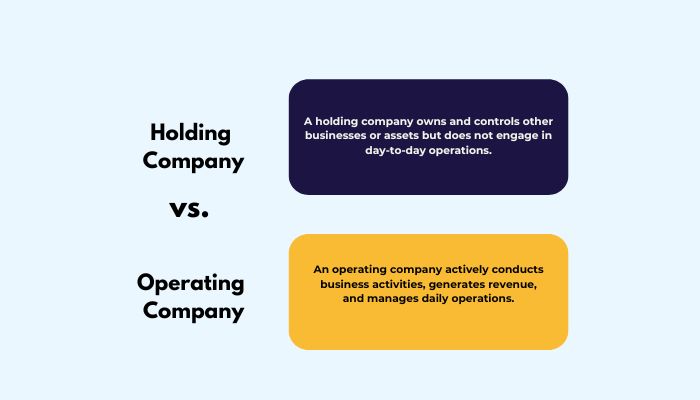

A holding company is essentially a business that exists to own other businesses. It doesn’t make products, provide services, or engage in the daily grind of satisfying customers or dealing with Karen from accounting. Instead, it holds equity in subsidiaries, manages intellectual property, and collects dividends like a dragon hoarding gold. In short, holding companies are legally and financially engineered to minimize liability while maximizing control over operating entities. They’re the puppeteers behind the curtain, pulling the strings while the operating companies dance for the audience. If you want the full breakdown of entity types, ownership layers, and how these structures are actually financially engineered, check out our complete guide on how holding companies work.

Structurally, holding companies are the apex predators of corporate design. They centralize strategic decisions, capitalize on tax advantages, and consolidate power—all while technically doing “nothing.” Yet somehow, they end up with all the assets when the dust settles. Funny how that works.

What Is an Operating Company?

Operating companies, on the other hand, are the ones getting their hands dirty. They are the entities out there manufacturing products, delivering services, managing employees, and dealing with the charming nuances of regulatory compliance. They’re the workhorses, or more appropriately, the cannon fodder, taking on the risk and liability while the holding company shelters itself in the background.

When you see a brand hustling in the marketplace, odds are you’re looking at an OpCo. They generate revenue, pay the bills, and occasionally make enough profit to send a modest dividend upstream to their beloved HoldCo overlords.

Ownership vs. Operation — Or Why Holding Companies Sleep Better at Night

Liability Containment (aka “Don’t Sue Me, Bro”)

One of the juiciest reasons for deploying a holding company is to lock your valuable assets away from the grubby hands of creditors. When lawsuits or debt collectors come knocking on the OpCo’s door, the HoldCo sits comfortably out of reach, cradling trademarks, patents, and real estate like prized possessions in a panic room. This separation ensures that if (read: when) the operating company runs afoul of litigation or financial disaster, the holding company’s asset stash remains untouchable.

It’s a beautiful arrangement: the operating company can take the hits, file bankruptcy if necessary, and the holding company can simply shift its gaze to the next acquisition, all while the plaintiff's attorneys seethe.

Tax Optimization Shenanigans

While operating companies are busy cutting payroll checks and remitting sales tax, holding companies are playing 4D chess with tax codes. By structuring ownership and revenue flows through the holding entity, savvy operators can mitigate tax burdens across jurisdictions. Holding companies can offset profits from one OpCo with losses from another, shuffle intellectual property royalties around like playing cards, and, in some cases, enjoy preferential tax treatment depending on the domicile.

Operating companies, meanwhile, get the honor of paying full freight on income taxes, employment taxes, and a parade of other government-sponsored headaches. It’s no wonder the holding company model is the darling of those with an affinity for legal loopholes.

Cash Flow Gymnastics: Dividends, Transfers, and Corporate Cartwheels

Moving Money Without Raising Eyebrows (Mostly)

A holding company’s job isn’t just to sit on assets; it’s also about moving capital efficiently without triggering alarms at the IRS or local tax authorities. Dividends are the tried-and-true method of getting profits from OpCo to HoldCo, but the magic comes in knowing how much to extract and when.

Too aggressive, and you risk leaving the OpCo undercapitalized, which courts tend to frown upon in bankruptcy proceedings. Too conservative, and you’re just sitting on idle cash that could be deployed elsewhere. The holding company walks a tightrope, ensuring funds are moved in a way that maximizes utility while minimizing exposure—preferably with a paper trail that makes even the nosiest auditor yawn with boredom.

Financing Flexibility (or How To Look Rich Without Actually Producing Anything)

Holding companies excel at leveraging the combined balance sheets of their subsidiaries to secure financing. Need a loan? Don’t worry. The HoldCo can pledge equity in five different OpCos as collateral without actually generating revenue itself. Banks love this. They get diversified risk, and you get capital without disturbing the operational focus of any single subsidiary.

Operating companies, on the other hand, often live and die by their cash flow statements. Their borrowing capacity is limited to their own performance, which makes them the financial equivalent of living paycheck to paycheck—albeit at corporate scale.

Risk, Reward, and Other Bedtime Stories for Capitalists

Why Holding Companies Love Bankruptcy (From a Safe Distance)

The dirty little secret of the holding-operating model is that bankruptcy can be a feature, not a bug. When an OpCo starts to tank, the HoldCo can strategically decide whether to fund a rescue or let the subsidiary sink into insolvency like a stone. Thanks to the structural separation, the holding company typically remains insulated from the carnage.

It’s almost poetic. The OpCo gets to take all the operational risks and absorb the market failures. Meanwhile, the holding company sheds its underperforming asset with minimal collateral damage. It's capitalism’s version of ghosting.

Scaling Without Sweating

Scaling a business organically is hard. Scaling through acquisitions via a holding company is, well, slightly less hard—assuming you enjoy M&A due diligence as a hobby. The HoldCo model allows for aggressive expansion without diluting focus. Rather than force a single operating team to manage disparate industries or geographies, you buy or build OpCos to handle the specifics.

Each OpCo gets its own leadership team, its own culture, and its own headaches. The holding company, meanwhile, orchestrates from above, ensuring capital flows where it’s needed and strategic alignment stays on track—all without worrying about the day-to-day grind of any one business unit.

So Which One Should You Build? (Hint: Yes)

Why the Smart Money Builds Both

Here’s the punchline: it’s not really about choosing one over the other. The best operators build both. You create a holding company to protect assets and optimize capital, and you launch operating companies to actually do the work. This dual structure provides flexibility, tax advantages, and insulation from risk—while positioning you as the puppet master of a thriving corporate empire.

If you’re only building OpCos, you’re leaving value on the table. If you’re only running a HoldCo without any real assets underneath, well... congrats on your empty shell. Balance is the name of the game.

Common Pitfalls (Or How To Accidentally Create a Tax Nightmare)

Of course, all of this only works if you keep your entities as separate as your work and personal email accounts. Commingling funds, overlapping operations, and sloppy documentation are the fast tracks to piercing the corporate veil—meaning the liability shield you worked so hard to build crumbles under legal scrutiny.

And, naturally, nothing delights tax authorities more than a holding structure done badly. Forget to dot your i’s or cross your t’s, and suddenly your clever dividend strategy becomes an all-expenses-paid audit.

Considering a transaction?

Speak with our team about an acquisition, partnership, or exit — in confidence.