Insight

Legacy Planning: Pairing CRTs With Life Insurance to Benefit Your Heirs

When you spend decades starting, acquiring, and building businesses under the umbrella of a holding company, the conversation eventually shifts from growth to legacy. It is one thing to amass an enterprise that deploys capital, time, talent, and technology; it is another to pass that value to the next generation in a tax-efficient, mission-aligned way

A pairing that often accomplishes both goals is the combination of a Charitable Remainder Trust (CRT) and strategically placed life-insurance coverage. Below is a practical, entrepreneur-friendly guide to how the two tools work together—and how they can keep more wealth in the hands of your heirs while continuing to advance the causes you care about.

Why Legacy Planning Deserves Founder-Level Attention

The Wealth-Transfer Puzzle for Business Builders

Many founders assume the sale of a portfolio company or a minority recap will automatically secure their family’s future. Yet once you factor in capital-gains tax, estate tax, state inheritance rules, and ongoing liquidity needs, the real after-tax value can shrink quickly. One eye-opening data point: the current federal estate-tax exemption is scheduled to fall by roughly half in 2026, placing significantly more of a growing estate within the IRS’s reach.

Why a Conventional Living Trust May Not Be Enough

A standard revocable living trust avoids probate and provides privacy, but it does not eliminate estate tax. If your holdings include rapidly appreciating stock or real estate, simply dropping everything into a living trust means heirs still inherit the built-in tax bill. A legacy structure that layers income tax and estate-tax minimization—plus a philanthropic element—often delivers a more durable solution.

CRTs 101: Income for You, Remainder for a Cause

| Feature / Goal | Charitable Remainder Trust (CRT) | Irrevocable Life Insurance Trust (ILIT) | Combined CRT + ILIT Strategy |

|---|---|---|---|

| Primary Purpose | Create income stream & support charity | Preserve inheritance for heirs | Maximize tax efficiency & dual legacy |

| Typical Assets Used | Appreciated stock, real estate, private business interests | CRT income or external funds used to pay premiums | Appreciated assets → CRT → income → ILIT premiums |

| Tax Benefits | ✓ Immediate income-tax deduction ✓ Capital gains tax deferral ✓ Estate-tax reduction |

✓ Tax-free death benefit ✓ Removes policy from taxable estate |

✓ All CRT & ILIT benefits ✓ Tax arbitrage opportunity |

| Income Stream | Yes — fixed (annuity) or variable (unitrust) | No direct income stream | CRT income funds life insurance premiums |

| Philanthropic Impact | Charity receives remainder of trust | None directly | Charitable giving + full family wealth replacement |

| Heir Benefit | None — remainder goes to charity | Heirs receive tax-free life insurance payout | Heirs receive payout equal to or greater than CRT contribution |

How a Charitable Remainder Trust Works

- Transfer highly appreciated assets—public stock, private shares, or even real estate—into an irrevocable CRT.

- Sell assets inside the trust without triggering immediate capital-gains tax because it is a tax-exempt entity.

- Receive an annual income stream—either a percentage of the trust’s value (unitrust) or a fixed dollar amount (annuity trust)—over a fixed term or lifetime.

- Distribute the remaining assets to a qualified charity when the term ends.

Major Tax Advantages

- Charitable deduction: Immediate income-tax deduction based on the present value of the remainder interest.

- Capital gains deferral: Assets sold in the CRT are not taxed at the time of sale, allowing reinvestment of the full pre-tax proceeds.

- Estate-tax reduction: CRT assets are removed from your taxable estate, reducing future estate exposure.

Life Insurance: The Heirs’ Replenishment Tool

Solving the “But What About My Kids?” Concern

The catch with a CRT is obvious: the charity, not the family, receives the remainder. Enter life insurance. By directing a portion of the CRT’s tax-advantaged income to premiums on a separate life-insurance policy—often held in an irrevocable life-insurance trust (ILIT)—you create a pool of tax-free death-benefit dollars specifically for heirs. In many cases the death benefit can equal or even exceed the value of the assets originally placed in the CRT.

Policy Design Choices

- Permanent policies: Whole life, universal life, or indexed universal life provide lifetime coverage and cash-value growth.

- Survivorship coverage: Insures both spouses and often delivers a larger benefit for the same premium, paid when estate liquidity is most needed.

Pairing CRTs With Life Insurance: Putting the Pieces Together

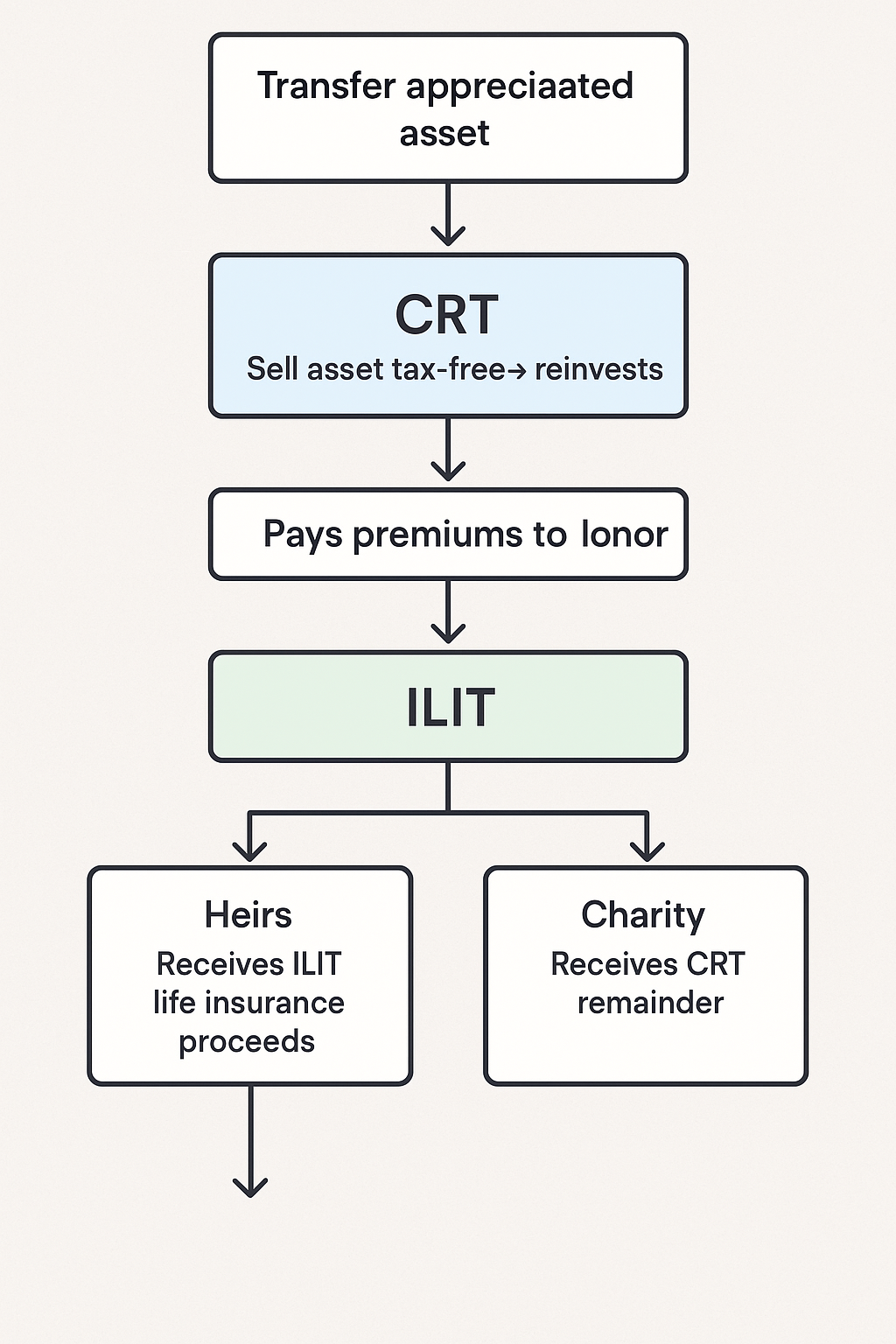

The Typical Flow

- Contribute appreciated assets to the CRT and claim a charitable deduction.

- Sell and reinvest through the CRT, which begins paying you income.

- Use income to fund premiums on a life-insurance policy held by an ILIT.

- Distribute benefits at death: heirs receive the life-insurance payout, and the charity receives the CRT remainder.

Key Benefits at a Glance

- Double impact: Charitable legacy plus full family-wealth replacement.

- Tax efficiency: Income-tax deduction, capital-gains deferral, estate-tax reduction, and tax-free insurance proceeds.

- Cash-flow flexibility: Adjust CRT payout and premium allocation to meet income needs.

- Asset protection: CRT and ILIT assets are generally shielded from creditors.

Practical Considerations and Common Pitfalls

Timing and Valuation Issues

- Early planning: Initiate CRT drafting before signing any LOI or sale agreements.

- Accurate valuation: Prevents IRS issues and ensures correct deduction sizing.

Picking the Right Payout Rate

- IRS compliance: The charitable remainder must be at least 10% of the trust’s value.

- Balance: Choose a rate that supports income needs without depleting the remainder too aggressively.

Trustee and Investment Oversight

- Trustee choice: Select someone with fiduciary experience, particularly for managing alternative assets.

- Complex portfolios: Ensure capability to handle K-1s, capital calls, and periodic private asset valuations.

Matching Policy Structure to Cash Flow

- Premium timing: Missing payments could cause policy lapse.

- Contract structure: Consider level-premium or limited-pay options for income alignment.

Implementation Roadmap

Assemble Your Advisory Bench

- Team structure: Coordinate estate attorney, tax counsel, insurance advisor, and investment manager.

- Unified planning: Make sure all work from shared projections to avoid blind spots.

Draft and Fund the Trusts

- CRT setup: Specify payout method, term, and chosen charity.

- ILIT formation: Include independent trustee and Crummey notices for compliance.

- Asset transfer: Move appreciated assets into CRT before the sale occurs.

- Premium funding: Use CRT income to pay insurance premiums through the ILIT.

Monitor, Rebalance, and Report

- Annual CRT review: Adjust based on growth or income needs.

- ILIT tracking: Ensure policy value and benefits stay on target.

- Estate updates: Reflect major life changes in legal documents.

Final Thoughts

A CRT-plus-life-insurance strategy delivers a rare triple play: it lets business owners harvest appreciation built under a holding company without a punitive capital-gains haircut, secures lifetime income and philanthropic impact, and restores—or even enhances—the inheritance earmarked for heirs. The planning details can feel complex, but the outcome is elegantly simple: more dollars flow to family and favorite causes, and fewer disappear to taxes or litigation risk.

If you have a liquidity event on the horizon or already sit on low-basis assets inside your operating or holding entities, now is the moment to run the numbers. Legacy planning done early is far less about legal documents and more about seeing opportunity where others only see obstacles. Assemble the right team, commit to a timeline, and turn decades of entrepreneurial effort into an enduring, tax-savvy legacy—one that honors both your heirs and the communities your business success has helped support.

Considering a transaction?

Speak with our team about an acquisition, partnership, or exit — in confidence.